Cash Flow & The Golden Goose

Live off the eggs. Don’t kill the goose!

When it comes to achieving financial independence, you must understand the difference between living off interest income and cutting into your assets/equity.

Do you remember the story of the goose that laid golden eggs?

On the brink of bankruptcy, a poor farmer and his wife found a very special goose with an incredible ability. Instead of laying regular eggs, this goose laid eggs made of solid gold. Each day they would take extra special care of the goose, ensuring he was well fed, well groomed and had plenty of nice soft grass to lay his eggs. Weeks went by and the goose continued to lay a golden egg each day. The farmer and his wife had begun selling the eggs and started to grow rather wealthy. They upgraded their house and farm, bought more land, more cattle and more tractors. Soon, the man and his wife became complacent with their new found wealth and thought the goose wasn’t laying the eggs fast enough. They supposed that he must contain a vast number of eggs inside, and decided by cutting him open, they could retrieve all the gold at once! So they killed him, cut him open, and to their dismay found that, inside, he was just a regular old goose after all. The foolish pair, hoping to become very rich all at once, deprived themselves of the gain of which they were assured day by day.

There is a certain belief in mainstream society that obtaining a “big lump sum of cash” means you’re set for life. If only you could make a few million dollars, then you could live freely and never work another day in your life, right?

Well, no, not necessarily!

Some people envisage a 7 figure bank account or a massive vault filled with cash that they can draw from until the day they die. This is another great misconception (or foolish use) of wealth. Sure, you can draw from your kitty, but it’s not wise. By doing so, you are slowly killing your very own golden goose. Besides, a million dollars doesn’t buy you that much these days. Even $10,000,000 drawn over 50 years is “only” $200k per year. Factoring for inflation, that $200k in 50 years from today will buy you the equivalent of just $60k in today’s terms.

The individual who does not learn to mobilize her cash and equity to turn it into an income stream will never achieve true financial independence. The best she can hope to do is slowly drain the pool of cash until it has all dried up.

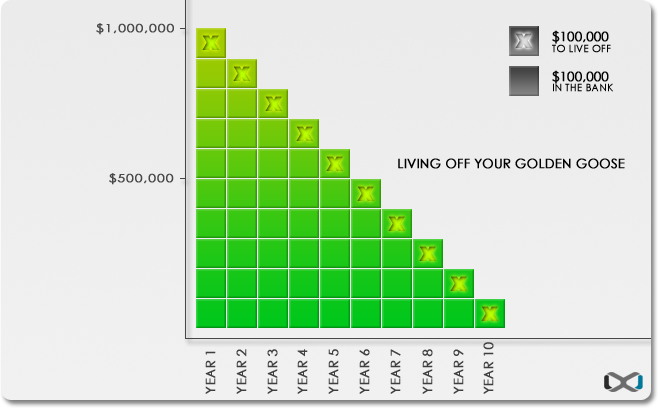

Example 1

Let’s say Neil stumbles across $1,000,000 which he decides to put in the bank and draw from.

He figures he could live pretty comfortably off $100,000 per year. The problem is that he could only survive for 10 years, then he’d have to go back to work! At just 3% pa, the hidden cost of inflation essentially steals another $30k per year from Neil due to the value of his dollar losing power. The truth is that if he had $1,000,000 in the bank, he could probably only actually last around 7 years.

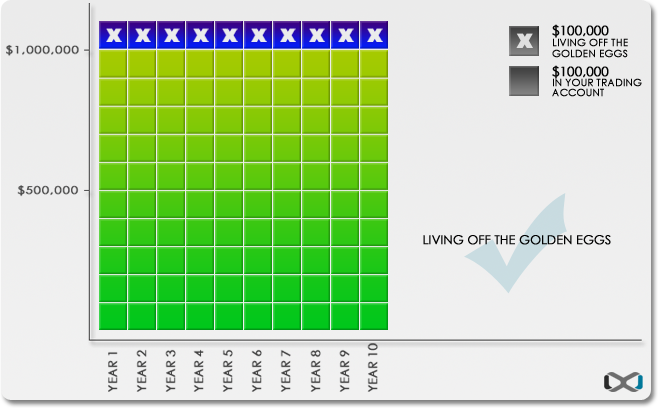

Example 2

Now consider Luke, who has also just stumbled across $1,000,000 which he decides to invest.

Luke only needs to generate a 10% annual return in order to generate his $100,000. This can afford him a comfortable lifestyle. Over the year, he has the same quality of lifestyle as Neil, but instead of cutting into his kitty, he lives on the returns instead. At the end of the year, Luke still has his $1,000,000 golden goose which produces $100,000 per annum.

He can (hypothetically) live off these returns comfortably for the rest of his life, and pass the golden goose on to his children and his children’s children.

Your cash accounts, savings, investment funds and trading accounts act as your golden goose, and cash flow is the eggs it produces.

Never kill your golden goose!

Put it to work and grow it big and strong so you can live off the eggs. Society tends to portray “net worth” as the real measuring stick of prosperity, however, those who have actually achieved financial prosperity realize that, in fact, it is their level of cash flow (income) that ultimately creates the most significant impact on their lifestyle.

Income is the outcome. From the point of view of lifestyle design, building your “net worth” is primarily a way to fatten your goose in order to produce bigger golden eggs.

An acquaintance of mine has amassed an impressive property portfolio of over $10 million, yet he struggles to pay for a nice dinner in town and cannot afford to fly business class during his travels. On paper, he’s amongst the wealthiest 0.5% on the planet. He has a high net worth tied up in non-liquid equity. As we teach at Infinite Prosperity, this style of wealth creation is certainly more empowering than staying broke, but it does not necessarily enable you to live a “millionaire lifestyle”.

On the contrary, we have traders and online business owners in this very community who have a very modest investment portfolio, yet are able to generate $10-15K cash flow per month. So who do you think leads a better lifestyle?

High Income = High Lifestyle

So then, should I just focus on income? Our advice is, take both! Start with high income first.

Hopefully, this section has highlighted a common misunderstanding – that a high net worth buys the luxury lifestyle. For the most part, it is in fact high income that buys the luxury lifestyle. If someone with a high net worth is unable to mobilize their wealth to create income, he or she may not necessarily be able to lead a great lifestyle.

Leave a Comment